Aspects of modern monetary theory

John Hermann

Following the advent of the global economic crisis, there has been a growing recognition and understanding of the claims made by a relatively recent school of economic thought known as Modern Monetary Theory (MMT), which is a development of what used to be called Chartalism. Considering that there are ongoing economic crises within both Europe and North America which relate directly to the issues addressed by MMT, it seems timely to look at some of MMT’s claims and how an MMT perspective might assist in resolving those crises. Firstly we will review money and government debt.

Two types of money

There are two widely used forms of money: (a) State fiat money, which is money created by a sovereign monetary authority (usually a central bank) and acceptable for the payment of taxes. The main forms being currency (coins & notes, which have been declared to be legal tender) and creditary banking reserves (exchange settlement funds); and (b) Bank credit money, which is money created by commercial depositories (banking institutions) as retail deposits, and exchangeable with legal tender.

There is an important subdivision of state fiat money, known as banking reserves, which is the conjunction of currency held by banking institutions and their deposits in the central bank. The two components of banking reserves are interchangeable. Currency held by the public is usually referred to as currency in circulation.

Central (sovereign) government debt

A government which is economically sovereign creates and issues the currency used by its citizens. And traditionally it also creates and issues securities, which are instruments of debt sold to the private sector on the open market. When government securities are sold to the non-bank private sector, money is extracted from the economy in exchange for another (generally liquid) financial asset, so that the financial wealth of the private sector remains unchanged.

MMT asserts that such public debt is fundamentally different to private debt, in that it is always possible for a government which issues currency to roll the debt over – in perpetuity – and to pay any interest due on that debt. According to MMT there is no constraint, at least in principle, on the ability of a sovereign government to effect such payment. For a sovereign government there is no “central government debt problem” as such, the latter term indicating a misunderstanding held by those with a poor understanding of macroeconomic principles.

Spending, taxing and borrowing

Contrary to what many neoclassical economists believe (and would have others believe), a sovereign government engages in taxing and borrowing only ostensibly for the purpose of raising revenue. Although central governments behave as if taxing and borrowing is undertaken in order to raise revenue, the MMT interpretation is that this is not what really happens. Thus government does not need to raise revenue for the purpose of funding specific cost items, because new money is injected into the economy whenever it spends.

Spending introduces new money into the economy, while taxing and borrowing remove money from the economy. Although at first sight there might appear to be a chicken-and-egg relationship in these fiscal flows, MMT asserts that the causal relationship is for spending to come first, and for taxing and borrowing to follow. If this relationship postulated by MMT is accepted, then it follows that the real and largely hidden purpose of taxing and borrowing is to recapture the money which a central (sovereign) government spends into the economy, in order (a) to keep a lid on inflation, and (b) to ensure that money moves around the economy with sufficient velocity.

Central government and the lower levels of government

The lower levels of government (state, provincial and municipal) do not issue their own currencies and – in Australia at least – do not impose income taxes on those whom they govern, although they are accustomed to imposing a range of other taxes, duties and levies. Their fiscal constraints are therefore quite different to those of the central government. A lower level of government – in common with the private sector – is obliged to be more careful in its budgeting than is a (sovereign) central government, which may safely run a budget deficit in perpetuity (and arguably should do so, according to MMT ideas).

Deficits are the norm

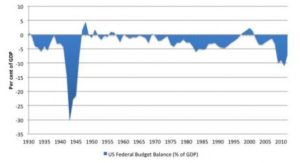

The following graph of the U.S. federal budget balance over 82 years (care of a blog by Bill Mitchell — http://bilbo.economicoutlook.net/blog/?p=22551) reveals that budgets have been in deficit for around 85% of the time. In other words, deficits are the norm and surpluses are the exception. I suspect that much the same picture would emerge with a more extended time-span. The history of budget balances indicates that the oft-held belief that running a sequence of budget deficits will have dire inflationary consequences for the economy is not grounded in reality. And MMT advocates insist that any drive to achieve a budget surplus in circumstances where there are idle resources and reduced aggregate demand is economic vandalism, because it leads to unnecessary austerity and can only hinder economic recovery.

Accounting conventions

Banking operates according to a set of accounting conventions, which are rules designed to match the receipt/loss of a certain type of asset by a banking institution (depository) with the receipt/loss of a liability of equal magnitude. The asset of particular concern is newly created bank credit money, which arises when a bank advances a new retail loan or when a cheque drawn on the central bank is deposited.

It is generally held by economists that banking reserves should be regarded as central bank liabilities. On the other hand, it may be argued also that it is inappropriate to attempt to make a central bank, as the creator and destroyer of state fiat money, conform to the accounting rules which apply to commercial banks.

Central government’s account with the central bank

Every central government maintains one or more accounts with its central bank. In Australia for example the federal government does its banking with the Reserve Bank of Australia (RBA). Thus the cheques written by an Australian government department are drawn on the RBA. The situation in New Zealand is a little different, as revealed by the following statement found in a part of the RBNZ website (http://www.rbnz.govt.nz/education/0114246.html):

Although the government ultimately does all of its banking with the Reserve Bank (via its Crown settlement account, or CSA), it uses an account held at Westpac for its transactions with the public. That’s why payments from the government, e.g. unemployment benefits, are paid using Westpac cheques. The transactions in this account are totalled up and the balance is transferred to the CSA at the end of the banking day.

The general account of a central government with its own central bank records in monetary terms the government’s various fiscal operations – specifically spending, borrowing from the private sector, tax receipts, and all other receipts. When a central government spends, its general account is debited accordingly. And when it borrows from the private sector or acquires tax (or other) receipts, its general account is credited accordingly.

There is general agreement that central government spending entails the creation of new retail demand deposits and an increase in the money supply (as measured by the monetary aggregate M1), while central government borrowing, taxing and the receipt of other income entails a reduction in the money supply. A more interesting issue is the fate of the banking reserves, which generally tag along with retail deposits in the broader economy. While the precise mechanics differs from country to country, in each case there exists some combination of (a) immediate removal of those reserves, in exchange for an increase in the government’s general account, (b) use of the reserves to temporarily purchase highly liquid (risk free) financial assets, and use of the reserves to temporarily create deposits in commercial banks (which deposits, however, lie outside the money supply M1). Items (b) and (c) are holding options, and those reserves are retrieved in a piecemeal manner as and when required according to the need to offset government spending operations, once again involving the removal of those reserves whenever the general account requires to be increased. The practice of maintaining holding investments and/or commercial bank deposits exists only for the purpose of regulating (minimising fluctuations in) the volume of banking reserves during the course of a financial year.

Are government deposits in the central bank money?

The economic mainstream hold that government entries or “deposits” in its own central bank account are a form of state fiat money, moreover one which is interchangeable with reserves. There is an alternative viewpoint, which is consistent with MMT ideas, which holds that such “deposits” are not money in any real sense of the word, but are merely accumulated credits in an operating account. An operating account records a financial reality, but it does not need to be regarded as a form of money. The rationale for this perspective is:

(a) One of the essential requirements of any entity which acts as money is that it is used by (traded, loaned and borrowed between) a sufficiently large number of marketplace players who have similar status and objectives in regard to those operations. Banking deposits in the central bank satisfy this criterion, since all of the players are in competition with each other with the common objective of maximising financial profit. In contrast, a central government maintains an account with its central bank for a quite different purpose, and its spending has a different objective, to that pertaining to commercial banks; and

(b) There are other examples within the financial system of accounts which are not regarded as being stores of spendable money, such as commercial banks’ internal operating accounts.

On this basis it may be held that the central government stands alone – that is, not in competition with any other entities possessing accounts with the central bank. Indicators of this difference lie in the fact that a central government sells bonds but never needs to buy bonds, and also borrows money but never needs to lend money. If all of this is held to be true then arguably the entries in the government’s general account are not money.

John Hermann is the ERA network editor