A thought experiment on budget surpluses

Steve Keen

While conservative parties – like the US Republicans, UK Tories, and Australia’s Liberals – are more emphatic on this point than their political rivals, there’s little doubt that all major political parties share the belief that the government should aim to have low government debt, to at least balance its budget, and at best to run a surplus. As the UK’s Prime Minister put it in 2013:

“Would you want a government that is not targeting a surplus in the next Parliament, that just said no, we’re going to run overdrafts all the way through the next parliament,” he told BBC political editor Nick Robinson.

“I don’t think that would be responsible. So the other parties are going to have to answer this question, ‘Do you think it’s right to have a surplus?’ I do.” (David Cameron: It’s responsible to target budget surplus”, BBC October 1, 2013)

So is it “right to run a surplus”? Let’s consider this via a little thought experiment. The numbers are far-fetched, but they’re chosen just to highlight the issue: Imagine an economy with a GDP of $100 per year, where the money supply is just $1 – so that $100 of output each year is generated by that $1 changing hands 100 times in a year. And imagine that this country’s government has accumulated debt of $100 – giving it a debt to GDP ratio of 100% – and it decides to reduce it by running a surplus that year of 1% of GDP. And imagine that it succeeds in its target.

What will this country’s GDP the following year, and what will happen to the government’s debt to GDP ratio? The GDP will be zero, and the government’s debt to GDP ratio will be infinite.

Huh? The outcomes of this policy are the opposite of its intentions: a policy aimed at reducing the government’s debt to GDP ratio increased it dramatically; and what is perceived as “good economic management” actually destroys the economy. What went wrong?

The target of running a surplus of 1% of GDP means that the country’s government collects $1 more in taxes than it spends. This $1 surplus of taxation over spending takes all of the money in the economy out of circulation, leaving the population with no money at all. The physical economy is still there, but without money, no-one can buy anything, and the economy collapses. The government can pay its debt down by $1 as planned, but the GDP of the economy is now zero, so the government debt to GDP ratio has gone from $100/$100 or 100%, to $99/$0 or infinity.

As I noted, the numbers are far-fetched, but the principle is correct: a government surplus effectively destroys money. A government surplus, though it might be undertaken with the noble aim of reducing government debt, and the noble intention of helping the economy to grow, will, without countervailing forces from elsewhere in the economy, increase the government’s debt to GDP ratio, and make the economy smaller (if the rate of turnover of money – it’s so- called “velocity of circulation” – is greater than one).

This thought experiment illustrates the logical flaw in the conventional belief that running a government surplus is “good economic management”: it ignores the vital relationship between government spending and the money supply. Unless the public finds some other way to compensate for the effect of a government surplus on the money supply, the surplus will reduce GDP by more than it reduces government debt.

But surely my thought experiment can’t be right, can it, because haven’t there been cases where governments have run surpluses and the economy has boomed? Yes there have been, because in the real world, the public can counter the destruction of money by a government surplus in two ways: they can borrow money from the banks, or they can run a trade surplus with the rest of the world (I’ll focus on a domestic economy here, leaving the impact of the trade balance for another article).

Just as a government surplus destroys money, lending by banks creates it (if new loans exceed the repayment of old loans by the public). Let’s extend our thought experiment to consider this possibility: Imagine that households and businesses in this hypothetical economy started with zero debt, and in the year that the government runs a 1% surplus, the public decides to go into debt to the banks to the tune of 2% of GDP, or $2.

What happens to the money supply, GDP, the government’s debt to GDP ratio, and the private sector’s debt to GDP ratio, the next year?

The total amount of money in the economy rises by $1 – minus $1 for the budget surplus, plus $2 from net lending by banks – and if the rate of turnover remains constant, then GDP will rise from $100 to $200. The government’s debt ratio will fall by more than it expected: debt will be cut from $100 to $99 as planned, but GDP will double to $200, so that the government’s debt ratio will fall by more than planned, from $100/$100 or 100%, to $99/$200 or 49.5%. But the private sector’s debt will rise from $0 (for a private debt ratio of $0/$100 or 0%) to 1% ($2/$200).

Of course, it’s possible that the rate of turnover of money will fall, because households and businesses now think that they should spend less, and save some money to enable them to repay their debt in the future. Let’s imagine that the turnover rate falls by 10% – from 100 times a year to 90. Then GDP rises from $100 (100 times $1) to $180 (90 times $2), which is not as good, but it still looks like a great economic success. The government debt ratio is $99/$180 or 55%, and the private sector’s debt ratio is $2/$180, or 1.11%.

With this outcome, everyone in the economy has exceeded their expectations: the government, which planned to reduce its debt ratio by 1% (from 100% of GDP to 99%) has instead reduced it by 45% (from 100% to 55%). GDP has increased by 80%, and the private sector, which planned for a debt ratio of 2%, has instead found itself with a debt ratio of just 1.1%. And the banks, which had no “skin in the game” before this year, end it with the non-bank public paying it interest on $2; with a 3% rate of interest, the banks earn $0.06. It ain’t much, but it’s better than nothing.

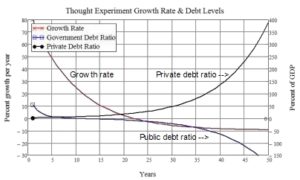

Such a favourable outcome elicits the obvious conclusion: if this worked so well in year 1, let’s do it again in year 2! So the second year of this experiment in “sound finance” goes like this: The government aims for a 1% surplus again – which is now $1.80. The private sector aims to borrow 2% of GDP again – which is $3.60. And the turnover rate falls again from 90 times a year to 81, as the private sector tries to save to allow debt repayment in future.

The outcome is: the money supply rises by $1.80 (the $3.60 created by the banks’ lending to the public, minus the $1.80 taken out of the economy by the government surplus) to $3.80; government debt now falls from $9 to $7; and with turnover at 81 times a year, GDP is now $307.80.

This more realistic thought experiment doesn’t alter the conclusion of the first – that a government surplus destroys money, and on its own would cause GDP to fall if the velocity of circulation of money was greater than one – but it shows that this process can be offset by private sector borrowing, and in the early days, the outcome looks really good.

But it doesn’t stay that way, because even though private sector borrowing keeps the money supply growing despite the government’s permanent surplus, the decline in velocity ultimately reduces GDP.

So how realistic is this thought experiment? It’s far from the sort of complete dynamic model that I prefer building, but the basic points it makes do apply in the real economy:

- Far from “saving money”, government surpluses actually destroy it;

- Absent a trade surplus, the only way to counter this is by the private sector borrowing as much as or more money into existence than the government destroys by its surplus;

- So an economy can grow if the government runs a surplus, but only at the expense of a rising private sector debt to GDP ratio; and ..

- As common-sense implies and history confirms, this can’t and won’t keep growing forever. At some point – for most countries, at between 150% and 250% of GDP – it stops growing. Then private sector deleveraging compounds the effect of a government surplus, also destroying money; finally,

- Velocity has had a secular tendency to fall since the 1980s, when private sector debt (in America) reached the significant level of 95% of GDP – see Figure 2. There’s every reason to think that this declining velocity has been in response to rising private sector indebtedness.

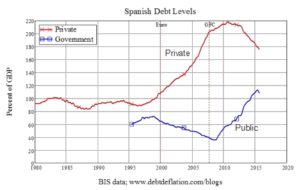

The unrealistic parts of this thought experiment relate to the ability of a government to run a surplus in the first place. Since both government taxation and government spending are to a large extent functions of the economy’s level of performance, governments that want to run surpluses can normally only do so when the economy is booming because of a rapid rate of increase in private debt. This was the secret to Spain’s period of government surpluses before the financial crisis, as Figure 3 vividly illustrates.

When the private debt bubble burst in the Global Financial Crisis and the private sector started to seriously de-lever, Spain’s government debt skyrocketed, despite the EU’s insane Maastricht Treaty rules (and this experience was replicated in virtually every OECD economy). Then attempts by the government to return to surplus by austerity caused the economy to shrink even faster.

So in answer to David Cameron’s question from 2013, “Do you think it’s right to have a surplus?”, my answer is “No, I don’t”– because unlike Dave, I understand that running a government surplus destroys money. The conventional belief that governments should run surpluses is not “sound finance”, but an unsound failure to understand capitalism.

Source: Forbes website http://www.forbes.com/sites/stevekeen/2016/03/13/a-thought-experiment-on-budget-surpluses/#13706cd431b1

This article has been reproduced with the permission of the author.

Dr Steve Keen is Professor of Economics and Head of the School of Economics, Politics and History at Kingston University in London, and is an ERA patron.