Will Private Credit have a ‘Minsky Moment’

Alan Prout

The Financial Review, Australia’s daily business paper, reported in November 2025 that the Australian Securities and Investment Commission (ASIC) was intending to pursue private credit funds suspected of breaking the law. A scathing surveillance report had recently called out hidden fees, aggressive marketing, and dubious valuation practices. ASIC chairman, Joe Longo, told the National Press Club that private credit faced its own ‘Minsky moment’, with a market collapse if the build-up of risks was not addressed (Financial Review, 2025). Since then, concern, not to say alarm, about private credit has proliferated globally. This is not confined to the financial media. Steve Keen (2026), for example, recently mentioned the growing size of private credit as one of the sources of debt buildup that could trigger a deep global recession. In Australia, private credit deals in the construction and commercial real estate sectors are seen as under particular strain, but globally stress is especially evident in technology – especially Artificial Intelligence (AI) and software investment.

But how realistic is the threat of a private credit crash? In particular, how likely is private credit to trigger a debt deflation event as described by Hyman Minsky? In exploring this question, I want to suggest that the evolving situation, whilst ultimately threatening, is also more complex and uncertain than these reports might suggest.

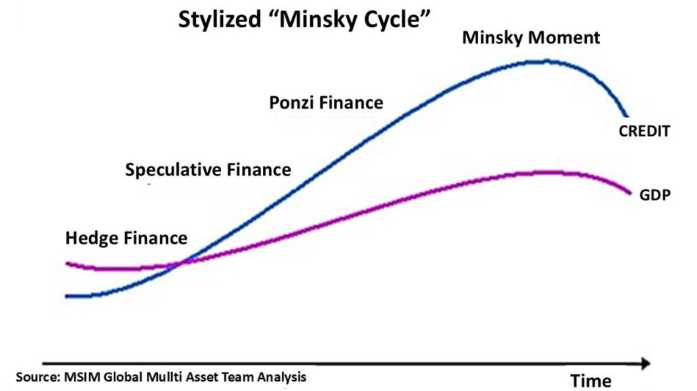

The term ‘Minsky moment’ denotes a sudden collapse in asset prices following a prolonged period of excessive lending and speculative investment. The term is named after the Keynesian economist Hyman Minsky, who in the 1980s showed that capitalist economies are inherently prone to instability because periods of economic calm encourage increasingly risky behaviour. In Minsky’s model, crises are not caused primarily by external shocks but are generated by markets moving through a cycle of three stages: first comes ‘hedge finance’ (where borrowers can repay both principal and interest), then ‘speculative finance’ (where they can only service interest), and finally, ‘Ponzi finance’ (where repayment depends on rising asset prices).

Minsky proposes that as confidence in a capitalist economy builds, leverage increases and risks are underestimated. In the final, ‘Ponzi’, stage the fragile structure breaks and borrowers are forced to sell assets to meet obligations, leading to falling prices, margin calls, and a cascade of further selling.

Liquidity evaporates, and what had appeared to be a stable system rapidly unravels. The Global Financial Crisis of 2007/8 is an exemplar. (For the detail and context of Minsky’s argument see Wray, 2026, especially Ch 3.)

The term ‘private credit’ refers to nonbank lending. Such lending is typically provided directly to businesses by pension funds, insurance companies, private equity firms, and other specialist lenders. Frequently, especially at the start of the cycle, these loans are to SMEs that may find it difficult to win loans from banks.

Crucially, these loans are not traded on public markets and are subject to far less regulatory oversight than bank lending. Their valuation is not subject to daily market fluctuations but to less frequent (often annual) mark-to-model (rather than mark-to-market) measures that may hide problems and misrepresent value for extended periods. The attraction of private credit to lenders is that it tends to command higher yields than traditional fixed income instruments, promising to compensate investors for lower liquidity, opaque and bespoke terms, and an overall higher credit risk.

Current concerns focus on the rapid increase in size of such private credit loans (Cai and Haque, 2024; Alternative Investment Management Association, 2025). These have grown dramatically during the past two decades.

Globally, private credit is estimated at US$40-50 billion in 2000, rising to roughly US$260 billion by 2009.

Growth accelerated after the Global Financial Crisis (GFC), reaching around US$1.7-2 trillion by 2023-24. By 2025, estimates place the market at approximately US$3.5 trillion, with continued strong annual expansion. Overall, private credit has expanded roughly seventy to eighty times since 2000 and about ten times since 2009, making it one of the fastest-growing segments of global finance.

However, worries are not simply to do with size; there are increasing signs that private credit funds are experiencing acute credit stress – the main reason that Longo issued the warning with which this article began. Rising defaults, with US private credit default rates reaching a record 9.2% in 2025 (Reuters, 2026a), are a clear case in point. Liquidity pressure is also building. For example, private credit firm Oaktree Capital Management faced 8.5% redemption requests in one of its credit funds in early 2026, forcing asset sales and dividend cuts (Reuters, 2026c).

At the same time, it is evident that lenders are sometimes effectively masking borrower distress by using payment-in-kind practices to defer interest payments (Reuters, 2026b), an indication of Minsky’s third phase of ‘Ponzi financing’, when interest payments due cannot be serviced. At some point, such stop-gap measures seem to betoken a higher risk of sudden failure, when reality catches up with accounting gimmicks. However, whilst increased risks are evident and real, voices from within the finance sector argue that expectations of imminent collapse are exaggerated. It is suggested that the very idiosyncrasy of private credit loan covenants can mean greater resilience and better risk management. Bespoke covenants do not have to be weaker than standard ones; they can offer stronger protections for investors. Lenders may also have a higher degree of involvement in and knowledge about borrowers’ businesses than do traditional bank lenders; they can see problems emerging earlier and respond with appropriate measures.

Another source of resilience is that private credit is typically less dependent on short-term funding than that originated by banks, and this could reduce the risk of sudden runs. Financial capital is largely locked up in closed-end funds, meaning managers are not usually forced to sell assets quickly to meet redemptions. Pension funds, for example, typically have long-term horizons and may be better positioned than traditional bank lenders to absorb temporary valuation swings without triggering fire sales.

These reassuring arguments are strengthened by comparing the size of current private credit with the mortgage debt just prior to the 2008 GFC. The difference in scale is significant. In 2008, US households carried a debt service ratio (the share of income that is used for repayments) of around 1516%. Such households today still have high debts but are relatively deleveraged, with a materially lower debt service ratio of 11-11.5%. As in 2008, mortgage debt still dominates, but unlike the previous era the creation of derivatives, the ‘financial weapons of mass destruction’ of which Warren Buffett famously spoke, are more limited. In 2008, US$ 1.2 trillion of mortgage debt supported US$ 5 trillion in synthetic Collateralised Debt Obligations, as well as Credit Default Swaps leveraged up to a monstrous US$ 62 trillion (Roberts, 2026). It was this amplification and obfuscation of debt instabilities through issuance of derivatives that substantially contributed to the systemic threat of 2007-8. And today, USD 1.7 – 2 trillion of private credit is large but has not (yet?) been significantly leveraged up in the creation of such derivatives.

Further solid reassurance also comes from a rather surprising source, the branch of economics to which Minsky himself can be assigned – Post-Keynesianism. Here, the key argument is that private credit is in principle quite unlike bank lending. A post-Keynesian analysis of private credit from the investment advice newsletter of Applied MMT (2026) sets out this case very clearly:

‘It really comes down to one critical distinction that almost nobody in mainstream macro-financial media is getting right . . the difference between endogenous money — the actual money-creation engine of the banking system — and what private credit is actually doing, which is something fundamentally different’ (Applied MMT, 2026).

Endogenous money creation is, of course, central to post-Keynesian economics, not least in the debt build up and deflation process described by Minsky. In its view, what matters is not the possibility of better risk management by private credit, and not the differences between the scale and distribution of Ponzi-financing now and in 2008, but a fundamental difference in the nature of the credit creation process.

So, is it game, set, and match to the conclusion that private credit, whilst a source of significant financial instability, is not at the moment a credible progenitor of a 2008-style Minsky moment? That would certainly follow if banks play no or little role in the creation of private credit. Put another way, the risk of contagion into the banking system from failures of private credit would seem relatively small if banks did not significantly expand their liability in the creation of private credit. And on the face of it, that would seem to be the case. After all, ‘private credit’ is defined primarily as ‘non-bank lending’, and as such is more akin to a friend lending you twenty dollars than a simultaneous expansion of assets and liabilities within a bank balance sheet. You might conceivably not pay the twenty dollars back (tut, tut!), but the default would stop with your friend.

Undeniably, there is a logic in favour of the Applied MMT argument, but unfortunately, in my opinion, it is not safe to draw the conclusion that private credit problems will avoid becoming systemic ones. The primary reason for this is that whilst a decade ago banks had very little involvement in private credit loans, that has changed in the last few years. The distinction between private credit and bank loans has become blurred in multiple ways. This means that although loans to companies are often originated by non-bank funds, a meaningful share of the funding chain still begins with commercial bank credit creation (Berrospide et al, 2025). Precise proportions are difficult to establish, because transparency and disclosure are poor, but several estimates suggest that bank-linked financing is substantial. US banks’ lending to non-depository financial institutions (NDFIs) reached nearly USD 2 trillion by 2025, with direct exposure specifically to private credit funds at roughly USD 300 billion (Berrospide et al., 2025). In Europe, Reuters (2024) estimates that 80% of new private credit funds in 2023 used bank-provided subscription lines. It is certainly arguable, then, that endogenous money creation has not disappeared but has migrated into more hidden layers in the structure of private credit.

It is, however, worth remembering the wider risk context of this process. As Keen (2026) states, the scope for crisis has been building for a long time and the catalyst for it is not necessarily single-stranded. In fact, candidates to trigger a downturn abound. One is to be seen in the US war on Iran and the trade restrictions operating in the Strait of Hormuz. According to Robert Pape (2026), the consequences of these will be immense and varied, running from chronic instability and commodity price inflation, to demand destruction and economic contraction.

Another possible trigger is the AI investment boom. This is estimated at USD 1.6 trillion since 2013, which means it is probably the largest technology investment wave in history. All such surges (from railways in the 1840s, through widespread electrification and automobiles in the 1920s and 1930s, to the dotcom era of the late 1990s) have passed through a period of overinvestment, leading to a bust (and, later, integration into the mainstream economy). Of the western companies vying for AI dominance, one, perhaps two or three at most, are likely to succeed. The rest will fail and it is possible they might all fail, beaten by the open-source alternatives being developed in China. Private credit is currently the fastest growing contributor to the AI boom, as funding has shifted from companies’ own cash flows to debt, where private credit plays a rapidly increasing role (Aldasoro, Doerr and Rees, 2026).

Overall, the risk of a Minsky-style debt deflation event seems to be growing but remains uncertain, in part because private credit’s workings are far from transparent. It is hard to say whether it alone could trigger a crisis or if some combination of different sectoral problems is needed to do so. In particular, it remains to be seen whether the number, density, and strategic importance of the connections between endogenous money creation by banks and private credit funds are enough to sustain real and significant contagion. Heterodox economics should remain alert to the risks.

References

Aldasoro, I., Doerr, S. and Rees, D. (2026) Financing the AI boom: From cash flows to debt, Bank of International Settlements, Bulletin 120. Switzerland: Basle. Available online at: https://www.bis.org/publ/bisbull120.htm. Accessed 2nd June 2026.

Alternative Investment Management Association (2025) Press Release: ‘Strong Growth sees Private Credit Market reach US$ 3.5 Trillion’. Available at: https://www.aima.org/article/press-release-strong-growth-sees-private-credit-market-reach-us-3-5-trillion. Accessed 1st April 2026.

Applied MMT (2026) Private Credit Isn’t 2008: Why the Headlines are Missing the Balance Sheet, Applied MMT Newsletter, April 20th, 2026. Available online: https://appliedmmt.com/private-credit-isnt-2008-why-the-headlines-are-missing-the-balance-sheet/. Accessed 2nd June 2026.

Basel Committee on Banking Supervision/Bank of International Settlements (2025) Banks’ interconnections with non-bank financial intermediaries. Available online: https://www.bis.org/bcbs/publ/d598.pdf. Accessed 31st May, 2025.

Berrospide, J., Cai, F., Siddhartha, L. and Zikes, F. (2025) Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications, FEDS Note, available online at: https://www.federalreserve.gov/econres/notes/feds-notes/bank-lending-to-private-credit-size-characteristics-and-financial-stability-implications-20250523.html. Accessed 31st May, 2026.

Cai, F. and Haque, S. (2024) Private Credit: Characteristics and Risks. Fed Note available online at: https://www.federalreserve.gov/econres/notes/feds-notes/private-credit-characteristics-and-risks-20240223.html. Accessed 1st April 2026.

Keen, S. (2026) Email on 2nd June 2026 to followers headed ‘A crack is Opening in the World Economy’ trailing a YouTube video ‘A Once in a Lifetime Crisis is Coming.’. Available online at: https://www.youtube.com/watch?v=OU-nDL7lDt8. Accessed 2nd June 2026.

Pape, R. (2026) “The Escalation Trap”, Professor Robert Pape’s official Substack, where he publishes essays such as “Why the Ceasefire Keeps Failing,” “Within 10 Days, Shortages Will Hit the Global Economy,” and “The Iran War Is About to Hit a Supply Wall—Markets Aren’t Ready.” Available online at: https://escalationtrap.substack.com/. Accessed 19th April, 2026.

Reuters (2024) Private credit ties to banks deepen in Europe as default risk rises. Available online at: https://www.reuters.com/business/finance/private-credit-ties-banks-deepen-europe-default-risk-rises-2024-03-14/. Accessed 31st May 2025.

Reuters (2026a) US Private Credit Defaults hit Record 9.2% in 2025 Fitch Says March 7th 2026. https://www.reuters.com/business/us-private-credit-defaults-hit-record-92-2025-fitch-says-2026-03-06/. Accessed 7th April, 2026.

Reuters (2026b) Private Lenders Delay Reckoning with Payment Concessions on Stressed Debt. March 31st 2026. https://www.reuters.com/business/finance/private-lenders-delay-reckoning-with-payment-concessions-stressed-debt-2026-03-31/ Accessed 7th April, 2026.

Reuters (2026c) Oaktree Fund meets 8.5% withdrawal requests as Redemptions Rattle Private Credit. https://www.reuters.com/business/oaktree-private-credit-fund-hit-by-surge-redemptions-2026-03-27/. Accessed 7th April 2026.

Roberts, L. (2026) Subprime 2.0: Will Private Credit Be the Trigger? https://seekingalpha.com/article/4886926-subprime-crisis-2-0-will-private-credit-be-trigger. Accessed 7th April 2026.

Wray, R.L. (2026) An Introduction to the Work of a Maverick Economist, Princeton/Oxford: Princeton University Press.

Editorial Comment:

Note that the term “private credit” used in this article refers to non-bank lending where the loaned money is not created. In the article, the author contrasts private credit with endogenous money creation. The meaning of “private credit” here should not be confused with that of the term “private sector debt” as used in the AI overview of Steve Keen’s work (see page 10 in this issue), meaning aggregate debt of the private sector. In the latter context, “credit” refers to the rate of change of net lending (or money creation by banks).