To make America great again, write off the private debt

Steve Keen

President Trump should pay no heed to what insider economists are telling him.

Dear President Trump,

Dear President Trump,

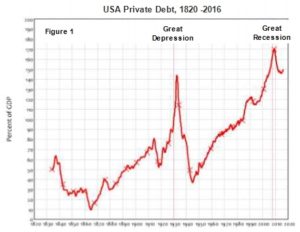

The key source of America’s economic weakness today is something you have experience with: private debt. All of the leaders before you have obsessed about government debt while ignoring private debt, which is far higher (150% of GDP versus 100%) and far more dangerous. You can do something about this, and unlike your purely political predecessors, your experience tells you that it can be done — the only question is how to do it.

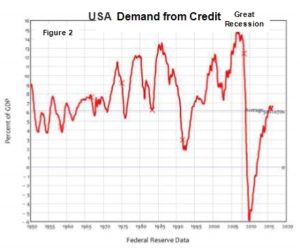

The private debt mound sitting on top of American households and businesses is the reason demand is depressed right now. With that debt mountain weighing them down, firms are reluctant to borrow and invest, while households are reluctant to use credit to consume. Credit demand is now back to the average of the 1950s to 1970s – the “Golden Age” of America, when your supporters today and their parents had well-paying manufacturing jobs. But it will easily turn negative again like it did during the Great Recession, given how enormous the debt burden still is today, since your immediate predecessor put more effort into rescuing Wall Street than he did into rescuing Main Street.

The Washington insider economists who are now going to attempt to get your ear will tell you that this private debt doesn’t matter, and that nothing can be done about it anyway. They’re wrong on both counts.

On whether it matters, they’ll say that one person’s debt is another person’s asset, so the total level of debt doesn’t matter. What they ignore is that banks create money and demand when they lend, and both money and demand fall when debt is repaid. They ignore the evidence shown in Figure 2, which I’ve been shoving in front of their faces for over a decade now (from early 2006, well before the Great Recession began).

On whether it can be done, they’ll tell you that this is “helicopter money”, and that it’s a dreadful idea. But the reality is that they’re doing it already. It’s just that the Fed’s helicopter, which they call “Quantitative Easing”, has been dropping that money on Wall Street rather than Main Street.

When the Fed buys bonds off a pension fund under QE, it creates the money that it buys that pension’s funds bonds with. The pension fund then does what pension funds do with money: they buy shares and other bonds. This drives up share markets, which benefits Wall Street and the 1% directly. Brokers get paid lots of commission, most of which they tend to stuff in their offshore bank accounts. They spend a fraction of this on Main Street, buying the odd hamburger.

But there would be far more money in Main Street’s hands if you put it there directly. There are many ways to do this, and it’s important to do it in a way that doesn’t favour people who borrowed over people who didn’t. The easiest way to illustrate it is to imagine that you tell the Federal Reserve to buy mortgages directly from the public.

For the Federal Reserve, there’s little practical difference to what it’s doing right now, except that 100% of the money it creates will turn up in Main Street bank accounts rather than those of Pension Funds and Wall Street brokers. With less debt, there’ll be more spending by Main Street, and, as a result, more employment. The only sufferers will be bankers and Wall Street, who will have far less income- earning assets than they have now, and may even have to work for a living.

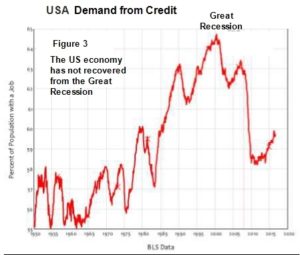

There will also be Washington economists, and Wall Street economists, and Federal Reserve economists, who will tell you that the economy is doing just fine now: just stick with current policies and everything will be OK. After all, isn’t the unemployment rate down to a mere 4.9% now, a boom-time level?

On this issue, your instincts are correct, and there’s official data to prove it: the employment rate shows that 3% less Americans are employed now than before the Great Recession. Part of that is demographic change, but most isn’t: 2 million less Americans aged 25-54 have a job now than had one in 2007.

You can rebuild America’s crumbling infrastructure too, because you can fund the rebuilding by running a deficit, with no fear of not being able to finance it – and here you’ll get as much mis- information from your Republican colleagues, obsessed with balancing the books, as you will do from the Washington consensus you seem to want to turn on its head. They’ll tell you that the Government can’t do that, because if it issues too many bonds the finance markets won’t buy them.

Yes they will. People buy American bonds because it’s America, and they accept payment in American dollars for those bonds for the same reason. And who produces those dollars? Effectively, the US government does now.

There are no practical limits to your capacity to produce them: it’s only the effect that matters. Good luck.

Reproduced with the permission of the author.

Source: Forbes, 9 Nov 2016 https://www.forbes.com/sites/stevekeen/2016/11/09/to-make-america-great-again-write-off-the-private-debt/#251f15ec73f8

Steve Keen is Professor of Economics at the Kingston University in London. Author of Debunking Economics and Can we avoid another financial crisis? Steve is also an ERA patron. Support Steve at https://www.patreon.com/ ProfSteveKeen if you like what he is doing.

Comment: Debts that cannot be paid will not be paid. Such debts must be restructured or forgiven and written off. In economics when this is done activity can proceed instead of being stifled. For this reason our bankruptcy courts do not engage in moralising to shame

debtors. It is irrelevant in that context. This applies to the rest of life. It doesn’t mean that we can’t fully engage in moralising. It just prevents moralising from making things worse, which it does often enough for those concerned to require awareness of the tendency to moralise.