The two least understood aspects of the European crisis

William K Black

Anyone who has analyzed the European crisis understands that it was not initiated by a “debt crisis” or a “spending” crisis. Nations like Ireland, Iceland, and Spain were being praised by ultra-conservative groups like Cato as the supposed exemplars of success of fiscal rectitude. By now, anyone who has analyzed the European crisis understands the pernicious role that the euro has played in the crisis because it is not a sovereign currency. By now, anyone who has analyzed the European crisis – including the IMF – knows that austerity has been a disaster that has caused a sharp contraction.

What even those who follow the European crisis are rarely saying, however, is the intersection of two facts about the crisis. First, the current European contraction is not a “recession” in many nations; it is an über- Depression. I explained in a previous article (referenced in the source link) that unemployment levels in much of Europe are roughly comparable to average unemployment rates in the largest European economies from 1930- 1938. Unemployment rates in the periphery are sometimes multiples of the average unemployment rates in the largest European economies during the Great Depression.

The EU, however, claims that there is merely a “mild recession.” The EU’s credibility is, unsurprisingly, in tatters. Unemployment in Greece and Spain is greater than peak U.S. unemployment during the Great Depression. The overall unemployment rate in the Eurozone is 12% – well over the U.S. unemployment rate in 1936, and half-again greater than the current U.S. unemployment rate. The unemployment rate in Portugal – which the EU claims as an almost success – is roughly twice the U.S. unemployment rate in 1936. Austerity has produced a depression in much of Europe, a depression so severe in several nations that it is worse than the Great Depression, and the Eurozone contraction is becoming more severe. The Eurozone depression was gratuitous – it did not have to happen. It is the product of economic dogmas that were discredited in 1937. We have taught economists for 75 years not to inflict austerity in response to a contraction.

Second, the troika (the EU, ECB, and the IMF) was insane to inflict austerity and cause the über-Depression, but the aspect that should scare us the most is that the troika generally inflicted considerably less severe austerity on the Eurozone than FDR inflicted on the U.S. in 1937. In 1937, FDR sought to reduce the budget deficit to 0.1%. The Eurozone runs a far larger average budget deficit – and that includes Germany. Even in 2013, Germany is targeting a 0.5% budget deficit. The Dutch are great deficit hawks, and they hope that there budget deficit will not exceed 3.3% this year (a level that exceeds what is supposed to be the EU limit). S p ain ’s deficit is over 10% because austerity has caused an unemployment rate roughly three times as large as our best estimates of the average unemployment rate in 1930-1938 in several large European nations. As nations like Spain inflict the austerity forced on them by the troika and are thrown into the über-Depression the GDP falls sharply enough that the budget deficit-to-GDP ratio often increases instead of falling.

The EU’s most recent economic forecast claims that austerity is growing more severe, so its models predict deficits will fall as a percentage of GDP. This might happen, but the EU models have consistently underestimated budget deficits because they have failed to predict that austerity will cause material falls in GDP and employment. Note that even under the assumption that austerity will succeed in reducing the ratio of budget deficits-to-GDP the EU expects the deficit ratio to be far higher than the 0.1% figure that FDR sought in 1937. “Since many Member States are implementing sizeable fiscal consolidation measures, the fiscal deficits are projected to decrease to 3.4% in the EU and 2.8% in the euro area in 2013.”

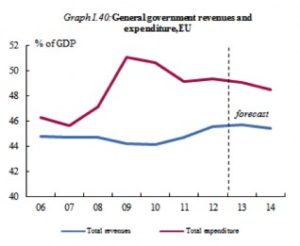

The same EU forecast provided historical information that shows graphically that the EU actually followed a fiscal policy of weak stimulus in 2008-2010 (see the top graph of total expenditure, in the following figure), which helped it begin to recover from the Great Recession. In 2010, however,

the EU switched to a fiscal policy of moderate austerity, which forced the eurozone back into recession by mid-2012.

Austerity is not simply a self-destructive policy – it is a weapon of mass economic destruction. The EU has managed to create the über-Depression through what was generally “only” moderate austerity. Unsurprisingly, it is the Nations that the troika forced to inflict the most severe austerity that are suffering the most severe depressions.

Source: Extracted from – http://neweconomicperspectives.org/2013/04/robert-reich-has-a-good-heart-but-an-inadequate-grasp-of-economics.html