Rethinking banking as a public franchise

Offering economists a more accurate metaphor – Tom Foster

Australians are very familiar with the concept of a franchise business, having the second highest number of franchising outlets per capita than any other country (ITA, 2022). When we think of franchises, some popular retail brands immediately come to mind; Jim’s Mowing, McDonalds and Harvey Norman to name several. So, what is meant by rethinking banking as a public franchise are we thinking about setting up a new franchise called Jim’s Banking? Not quite.

In their 2017 Cornell Law School paper The Finance Franchise, authors Robert C. Hockett and Saule T. Omarova (Hockett & Omarova, 2017) “map a new vision” (Ibid, 2017, p1211) of a nation’s financial system by asking for “re-conceptualization of modern finance as a hybrid publicprivate franchise system” (Ibid, 2017, p1149).

The authors commence by setting out the “three ways in which finance can originate and flow” (Ibid, 2017, p1143), the first two ways being:

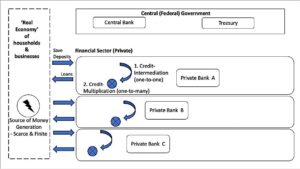

1. The Credit-Intermediation (or oneto-one) Model where bank deposits of private saver’s pre-accumulated funds are ‘recycled’ -one-to-one -in order to create loans for the bank’s lending customers. “This is the essence of the so-called “loanable funds” model of banking, pursuant to which “deposits make loans”” (Ibid, 2017, p1159); and

2. The Credit-Multiplication (known as one-to-many) Model, also commonly known as “fractional reserve banking” (Ibid, 2017, p1152), where funds lent out or invested by banks “constitute a multiple of (pre-accumulated) funds originally supplied by private savers” (Ibid, 2017, p1153).

As illustrated in Figure 1 the above two models reflect the “orthodox” (Ibid, 2017, p1151) view of a financial system operating independently to the public sector in which finance sector entities “compete” (Ibid, 2017, p1143) for a finite and “unavoidably scarce” (Ibid, 2017, p1145) amount of money “first accumulated in private hands” (Ibid, 2017, p1145).

The third model the authors set out is:

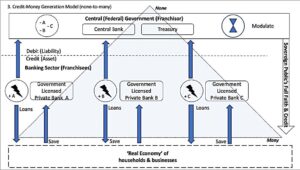

3. The Credit-Generation (or none-tomany) Model where money is not recycled or multiplied from pre-accumulated sources but instead, in the formation of a debt, is created from ‘nothing’ as a form of credit-money. This model reflects the “credit theory of money” where “money is credit and nothing but credit” (Mitchell Innes, 1913) and becomes, not a scarce and finite “creation” of the private sector, but an abundant and (potentially) infinite resource of the “state” (Keynes, 1930, p4).

To identify which of these models are used by banking in practice, some authors examine bank’s assets and liabilities reflected in their balance sheets, and “as a matter of accounting” are able to show (Hockett & Omarova, 2017, p1160):

1. The credit-intermediation (the loanable funds theory) model “to be false” (Ibid, 2017, p1158); instead “deposits do not make loans, but loans make deposits” (Ibid, 2017, p1161); and

2. The credit-multiplication (fractional reserve banking) model as “not necessary” (Ibid, 2017, p1160). In other words, the authors establish the way finance originates and flows throughout banking is that of credit-money produced by the credit-generation model. From this evidence the authors then use the credit nature of money to explain how “the public enters the realm of finance” (Ibid, 2017, p1155) through the public underwriting of these credit-generation operations by the private banks.

Replicating a function otherwise solely reserved for a sovereign government, (government licenced) private banks are authorised to conduct credit-generation operations in a nation’s sovereign (national) currency, thus creating credit-money in “immediately spendable form” (Ibid, 2017, p1156) for its clients to use. In the generation of credit-money (asset) an equivalent debit (liability) is always created and it is from this feature the authors identify two ways the government acts as guarantor (Ibid, 2017, pp1147-1148):

1. Accommodation – taking on the liability created by private banks in the generation of credit-money; and

2. Monetisation – The government recognising the “spendability” by bank customers of the credit-money that the government licences the private banks to generate.

These “twin acts” (Ibid, 2017, p1156) of accommodation and monetisation the authors define as the sovereign public’s full faith and credit that establishes the essential role played by the public sector in the credit-money that originates (is generated) and flows throughout the banking sector.

Comparing this hybrid public-private relationship to existing business models, the authors identify strong parallels with the franchise business model, observing the government acts as “defacto” (Ibid, 2017, p1156) franchisor with the government licensed private banks the franchisees.

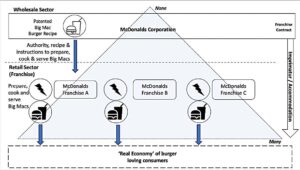

In a typical franchise agreement, the franchisor takes on the risk (accommodates) of licencing franchisee owned businesses to replicate the franchisor’s brand and ‘proven’ business system, which by following;

1. The franchisor can confidently provide its imprimatur that products and services franchisee customers consume are consistent with the franchisor’s brand and meet its quality specifications; and

2. Franchisees should be able to replicate the business results of the franchisor’s ‘promise’ of profits.

For example, McDonald Inc accommodates McDonald store franchisees who by following the McDonalds ‘prescribed’ system – cook and sell replicable Big Mac hamburgers which are already proven to be popular and profitable. By the franchisee following its proven system, McDonalds Inc can assure store customers they are consuming a Big Mac to McDonalds Inc specifications (i.e. consuming Big Mac Burgers made to MacDonald Inc’s patented Big Mac burger recipe). Also, the franchise owner by following the prescribed system is more likely to be rewarded with a profitable McDonald’s franchise business. Refer to Figure 2.

Using the public franchise lens to view banking, the sovereign government’s central bank and Treasury (typically) combined (Ibid, 2017, p1157) act as franchisor by issuing banking licences (aka franchise agreements) to the privately owned banks (franchisees), authorising those private banks to replicate the credit-generation of the nation’s credit-money. With franchisee banks acting according to the licensing process, the sovereign government is then able to guarantee accommodating the debit (liability) and the ‘spendability’ by these bank’s customers of the credit-money the banks create (monetisation). Refer to Figure 3.

In this way, backed by the sovereign public’s “full faith and credit”, and with the government in an oversight and credit modulator role, a nation’s creditmoney is propagated and allocated by the private banks to where the credit is needed by the ‘real’ economy (represented by businesses and households) (Ibid, 2017, p1211). The intended purpose of having this public-private hybrid, given that the licensed private banks compete between each other, is that the private banking sector will perform the tasks of issuing, circulating and distributing money more effectively and efficiently than the public sector could achieve.

Rethinking banking in this way as a public franchise has profound implications for public policy development. Of particular significance is the choice of macroeconomic theory for determining national policies, as a public franchise model exposes as inaccurate numerous aspects of the orthodox economic theory of banking and money. A contending replacement is Modern Monetary Theory (MMT), which incorporates within its foundations the credit theory of money (Mitchell et al., 2019, pp154155).

Another implication is that the private banking system is now recognised as a tool for public rather than for purely private purpose. To illustrate, the authors Hockett & Omarova use the example of ‘dysfunction’ (Hockett & Omarova, 2017, p1213) and financialisaton’ (Ibid, 2017, p1211) within many modern economies creating a capital ‘glut’ (Ibid, 2017, p1214) for the financial sector at the expense of the real economy. The authors argue the “attitudinal shift” (Ibid, 2017, p1216), created by viewing banking as a public franchise, would ensure efficient propagation and fairer allocation of the public’s credit-money towards supporting more productive uses across society.

References

1. Hockett, R.C & Omarova, S.T. (2017). The Finance Franchise. Cornell Law Review 102, pp 1143-1218. https://scholarship.law.cornell.edu/cgi/viewcontent.cgi?article=2660&context=facpub

2. International Trade Administration (ITA) (2022, July 19), Australia Country Commercial Guide, Franchising https://www.trade.gov/country-commercialguides/australia-franchising

3. Keynes, J.M. (1930). The Treatise on Money. Cambridge University Press http://tankona.free.fr/keynescw5.pdf

4. Mitchell, W., Wray, L. R., & Watts, M. (2019). Macroeconomics. pp154-155 MacMillian Education Limited

5. Mitchell Innes, A. (1913) “What is Money?” Banking Law Journal, May: pp377-408.

Tom Foster holds a Bachelor of Engineering (Electrical) Honours degree from the University of NSW, a Post Graduate Diploma in Management from MGSM and is currently studying for the Master of Economics of Sustainability degree at Torrens University.