Memo to mortgagors…get your house in order – John Kelly

Whether you believe it or not, an economic tsunami is coming and if you think we will survive the damage and the fall-out, as we did the GFC, you’re dreaming.

The next GFC will make the last one look like a vicarage fund raiser. Why? Because we are not just making the same mistakes as last time, we are making bigger ones.

One simple statistic reveals a frightening scenario. Currently, the big four banks have a combined equity of about

$162 billion. Place that along-side their current exposure to domestic mortgage loans of $1.6 trillion and you begin to see the looming threat.

Those mortgage loans have been fuelling an unsustainable housing bubble. But the banks see that as secondary to ensuring their share prices are maintained. What they seem oblivious to, is the plethora of business loans outstanding that feed off household demand.

The early warning signs are there. Stagnant wage growth is restricting spending and slowing demand. House- hold spending is becoming highly selective, limited to essentials but still relying on credit card financing. Our economy, all economies, are reliant on consumer spending. When consumers stop spending, the economy stops moving.

We have ignored the warnings, we have been seduced by low interest finance, cheap money and banks ever eager to lend at levels well beyond responsible management. As a result we have now reached the point when irrational expectation meets unmanageable debt.

As matters stand today, it’s not so much a case of the economy not moving, soon, the inevitable job losses will start to mount.

As with the GFC, the prime mover is the housing bubble. Let us be clear here. We are not talking about sovereign debt, what our national government has issued in bonds. That is always serviceable.

We are talking about what consumers owe and what is about to happen when it becomes apparent that they can no longer meet their debt obligations. We are talking about mortgage defaults.

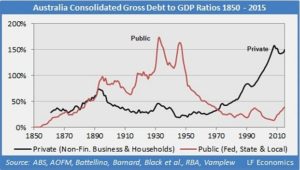

Look at the chart sourced from the Australian Bureau of Statistics, the AOFM, the RBA and others.

Australia’s current household debt to GDP is currently at 123 per cent, the second-highest in the world behind Switzerland. It has a household debt-to- income ratio at an all-time peak of 189 per cent. Mortgage loans to borrowers amount to more than six times house- hold incomes and could wipe out 20 per cent of the major banks’ equity base.

When the banks begin to see rising levels of mortgage default they will react without mercy. Foreclosures will follow, leading to a glut of homes for sale as the banks try to recover their money. House prices will crash. And that is just the start.

Businesses reliant on a strong, stable vibrant housing environment will feel the fall in sales of consumer goods. Unemployment will rise quickly leading to further decline in demand. From there, it’s all downhill.

The question then arises. What will this government do about it? If you think they will react the same way Kevin Rudd’s government acted, forget it. They will not. Their aversion to sovereign debt far outweighs any interest in issuing more debt.

The banks will demand the government protect their equity with guarantees and possibly a round or two of quantitative easing. That will save the banks but it won’t stop falling demand, businesses failing and higher levels of unemployment.

We, the consumers, the lifeblood of the economy will be left to fend for our- selves. That is the way of conservative governments. They look after their own. If we are reduced to soup kitchens and charitable handouts, so be it.

This government would rather give a company a tax break than stimulate an economy with direct debit consumer grants. So here is a warning. Get your house in order. Reduce your debt burdens. Pay down your credit card and look for a cheaper house with a lower mortgage if you can.

When the value of your four bedroom, double garage with swimming pool falls below the level of your mortgage, the bank will come knocking on your door. Better you act first. In situations where the inevitable is all too obvious, you have one option: be first.

If you would like a broader overview of the impending tsunami, read Nassim Khadem’s recent article in The Age [1]. When the spaghetti hits the fan and you decide it’s time to capitalise by selling your home for something less ostentatious, it will be too late.

Source: John Kelly, AIM ntwk, 9 Oct. 2017 https://theaimn.com/memo-mortgagees-get-house-order/Khadem, Nassim, Ten years since the global financial crisis, world still suffers ‘debt overhang’ http://www.theage.com.au/business/the-economy/10-years-since-the-gfc-20170526-gwe5f2.html