A modern Jubilee

Steve Keen

Michael Hudson’s simple phrase that “Debts that can’t be repaid, won’t be repaid” sums up the economic dilemma of our times. This does not involve sanctioning “moral hazard”, since the real moral hazard was in the behaviour of the finance sector in creating this debt in the first place. Most of this debt should never have been created, since all it did was fund disguised Ponzi Schemes that inflated asset values without adding to society’s productivity. Here the irresponsibility – and Moral Hazard – clearly lay with the lenders rather than the borrowers.

The only real question we face is not whether we should or should not repay this debt, but how are we going to go about not repaying it? The standard means of reducing debt – personal and corporate bankruptcies for some, slow repayment of debt in depressed economic conditions for others – could have us mired in deleveraging for 15 years, at its current rate (see Figure 1).

That fate would in turn mean one and a half decades where the boost to demand that rising debt should provide – when it finances investment rather than speculation – will not be there. The economy will tend to grow more slowly than is needed to absorb new entrants into the workforce, innovation will slow down, and justified political unrest will rise – with potentially unjustified social consequences. We don’t need to speculate about the economic and social damage such a future history will cause – all we need do is remember the last time.

We should, therefore, find a means to reduce the private debt burden now, and reduce the length of time we spend in this damaging process of deleveraging. Pre-capitalist societies instituted the practice of the Jubilee to escape from similar traps (Hudson 2000; 2004), and debt defaults have been a regular experience in the history of capitalism too (Reinhart and Rogoff 2008). So a prima facie alternative to 15 years of deleveraging would be an old- fashioned debt Jubilee.

But a Jubilee in our modern capitalist system faces two dilemmas. Firstly, in any capitalist system, a debt Jubilee would paralyse the financial sector by destroying bank assets. Secondly, in our era of securitized finance, the ownership of debt permeates society in the form of asset based securities (ABS) that generate income streams on which a multitude of non-bank recipients depend, from individuals to councils to pension funds.

Debt abolition would inevitably also destroy both the assets and the income streams of owners of ABSs, most of whom are innocent bystanders to the delusion and fraud that gave us the Subprime Crisis, and the myriad fiascos that Wall Street has perpetrated in the two decades since the 1987 Crash.

We therefore need a way to short-circuit the process of debt-deleveraging, while not destroying the assets of both the banking sector and the members of the non-banking public who purchased ABSs. One feasible means to do this is a “Modern Jubilee” – also describable as “Quantitative Easing for the public”.

Quantitative Easing was undertaken in the false belief that this would “kick start” the economy by spurring bank lending.

And although there are a lot of Americans who understandably think that government money would be better spent going directly to families and businesses instead of banks – “where’s our bailout?,” they ask – the truth is that a dollar of capital in a bank can actually result in eight or ten dollars of loans to families and businesses, a multiplier effect that can ultimately lead to a faster pace of economic growth. (Obama 2009, p. 3; emphasis added).

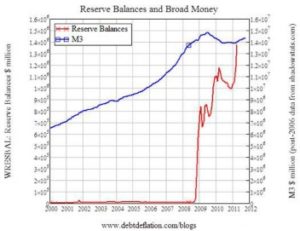

Instead, its main effect was to dramatically increase the idle reserves of the banking sector while the broad money supply stagnated or fell, (see Figure 2), for the obvious reasons that there is already too much private sector debt, and neither lenders nor the public want to take on more debt.

A Modern Jubilee would create fiat money in a like manner to Quantitative Easing, but would direct that money to the bank accounts of the public with the requirement that the first use of this money would be to reduce debt. Debtors whose debt exceeded their injection would have their debt reduced but not eliminated, while at the other extreme, recipients with no debt would receive a cash injection into their deposit accounts. The broad effects would be:

-

Debtors would have their debt level reduced;

-

Non-debtors would receive a cash injection;

-

The value of bank assets would remain constant, but the distribution would alter with debt-instruments declining in value and cash assets rising;

-

Bank income would fall, since debt is an income-earning asset for a bank while cash reserves are not;

-

The income flows to asset-backed securities would fall, since a substantial proportion of the debt backing such securities would be paid off; and

-

Members of the public (both individuals and corporations) who owned asset-backed- securities would have increased cash holdings out of which they could spend in lieu of the income stream from ABS’s on which they were previously dependent.

Clearly there are numerous complex issues to be considered in such a policy: the scale of money creation needed to have a significant positive impact (without excessive negative effects – there will obviously be such effects, but their importance should be judged against the alternative of continued deleveraging); the mechanics of the money creation process itself (which could replicate those of Quantitative Easing, but may also require changes to the legal prohibition of Reserve Banks from buying government bonds directly from the Treasury); the basis on which the funds would be distributed to the public; managing bank liquidity problems (since though banks would not be made insolvent by such a policy, they would suffer significant drops in their income streams); and ensuring that the program did not simply start another asset bubble.

References

1. Hudson, M. (2000). “The Mathematical Economics of Compound Interest: A 4,000- Year Overview.” Journal of Economic Studies 27(4-5): 344-363.

-

Hudson, M. (2004). The Archaeology of Money: Debt versus Barter Theories of Money’s Origins. Credit and state theories of money: The contributions of A. Mitchell Innes. L. R. Wray. Cheltenham, U.K, Edward Elgar: 99-127.

-

Obama, B. (2009). Obama’s Remarks on the Economy. New York, New York Times.

-

Reinhart, C. M. and K. S. Rogoff (2008). This Time is Different: A Panoramic View of Eight Centuries of Financial Crises, National Bureau of Economic Research, Inc, NBER Working Papers: 13882.

Source: Steve Keen’s Debtwatch ( http://www.debtdeflation.com/blogs/ )