Superannuation is complicated

A guaranteed government income in retirement would be simpler – Brendan Coates and Joey Moloney

Stress prompts many to under-spend superannuation

For the first time, many Australians are entering retirement with significant super balances: Australians are retiring with an average super balance of more than A$200,000, and couples with about $300,000.

Despite having saved enough to be comfortable, four in five people say planning for retirement is complicated, and 60% don’t think their retirements will be financially stress-free.

Few retirees draw down on their retirement savings as intended. In reality, many are actually net savers – their savings continue to grow for decades after they retire.

Our analysis of the ABS Survey of Income and Housing shows that for those aged 60-64 in 2003-04, average super balances had grown by 37% in real terms by the time they were aged 76-80 in 2019-20.

And their average net wealth, which excludes the equity in their home, grew by 14% over the same period.

Australia’s $4 trillion compulsory superannuation system is turning into a massive inheritance scheme. That’s not how super was intended to work.

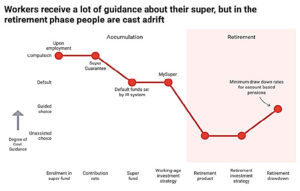

Retirees are given too little guidance

The super system makes most big decisions for working Australians, such as how much to contribute or how it’s invested. But upon retirement little guidance exists on how to use our funds.

More than 4 in 5 retirees are steered into account-based pensions. But partly because they’re anxious not to out-live their savings, this group manages their spending very cautiously.

While on average, an Australian woman aged 65 today can expect to live until age 88, they also have a one-in-five chance of either dying before age 81 or of making it to age 94.

And half of those retirees who use an account-based pension draw their super at the legislated minimum rates, which if followed, leaves 65% of super balances unspent in accordance with average life expectancy.

This widespread use of account-based pensions makes Australia a global outlier. Retirees in most rich countries are automatically given – or otherwise strongly encouraged to choose – an income guaranteed to last their entire lives.

Research suggests having an income that is guaranteed to last until death can reduce stress and boost retirees’ spending.

Government could steer retirees into annuities

Our report argues retirees should be encouraged to use 80% of their super balance above $250,000 to purchase an annuity.

The government could embed this pre-set guidance throughout the retirement income system. It could be included in all relevant communications with retirees from super funds, and especially at the point of retirement.

Research shows that retirees tend to choose the option put in front of them.

The remaining super balance — $25K,

plus the remaining 20% of any savings

above that level – would continue to be drawn down via an account-based pension. Retirees would still have to access their super for large purchases if needed.

Using some super to buy an annuity could boost expected retirement incomes by up to 25%, compared to solely drawing on an account-based pens-ion at legislated minimum rates.

And it would ensure that the bulk of retirees’ incomes, irrespective of their super balances, would be guaranteed to last the rest of their lives.

Annuities should be provided by government, not super funds

But steering retirees into annuities offered via super funds is unlikely to work.

Super funds have resisted previous attempts by government to require them to offer annuities to retirees.

Many people also struggle to understand and compare annuities. They oft-en find it difficult to switch to a better deal later even if they can spot one.

Recent experience in the UK showed when required to purchase an annuity, most people simply took what their fund was offering and often got a poor deal.

Designing a regulatory regime that overcomes these issues is a huge challenge. The best option, therefore, is for the government to directly offer annuities. It should offer all retirees a simple lifetime annuity as the baseline option.

The government could also offer alternatives including investment-linked annuities, where payments are guaranteed for life, but payments could vary based on investment returns.

Priced fairly, and managed by an independent agency, a government annuity would encourage their take-up. Retirees would be more confident that they’re getting a good deal.

The annuity payments could be made from the pool of capital created by the annuity purchases.

Under reasonable assumptions we project the government annuity provider could be managing assets totalling 2.5% of GDP by 2040.

Superannuation offers Australians the promise of a more comfortable and stress-free retirement. Government-offered annuities can help turn that dream into reality.

Esther Suckling made substantial contributions to the research underpinning this article. Republished under creative commons licence. The references indicated by underlining are accessible from the source.