Is 2021 Public Banking’s Watershed Moment?

Ellen Brown [1]

This article by Ellen Brown highlights the existence of U.S. legislative bills that have recently appeared in California and several other states, including New York, designed to authorise the formation of public banks by cities and counties, along the lines of the very successful public bank Bank of North Dakota (BND). Those new public banks will in turn provide public agencies access to loans at interest rates much lower than they could find at private banks. The California governor, Gavin Newsom, has already signed that state’s Public Banking Act (AB 857).

A few months into 2021 saw a flurry of public banking activity. Sixteen new bills to form publicly-owned banks or facilit- ate their formation were introduced in eight U.S. states during January and February. Two bills for a state-owned bank were introduced in New Mexico, two in Massachusetts, two in New York, one each in Oregon and Hawaii, and Washington State’s Public Bank Bill was re-introduced as a “Substitution”. Bills for city-owned banks were introduced in the cities of Philadelphia and San Francisco, and bills facilitating the formation of public banks or for feasibility study were introduced in New York, Oregon (three bills), and Hawaii.

In addition, California has now introduced a bill for a state-owned bank, and New Jersey is moving forward with a strong commitment from its governor to implement one. At the federal level, three bills for public banking were also introduced last year: the National Infra- structure Bank Bill (HR 6422), a new Postal Banking Act (S 4614), and the Public Banking Act (HR 8721).

As Oscar Abello wrote on NextCity.org in February, “(the year) 2021 could be public banking’s watershed moment. Legislators are starting to see public banks as a powerful potential tool to ensure a recovery that is more equitable than the last time.”

Why the surge in interest?

The devastation caused by nationwide Covid-19 lockdowns in 2020 has high-lighted the inadequacies of the current financial system in serving the public, local businesses and local governments.

Nearly 10 million jobs were lost to the lockdowns, more than 100,000 businesses were closed permanently, and a quarter of the entire population remains unbanked or underbanked. More than 18 million people are currently receiving unemployment benefits, and moratoria on rent and home foreclosures are due to expire this spring.

Where was the Federal Reserve in all this? It poured out trillions of dollars in relief, but the funds did not trickle down to the real economy. They flooded up, dramatically increasing the wealth gap. By October 2020, the top 1% of the U.S. population held 30.4% of house- hold wealth, 15 times that of the bottom 50%, which held 1.9% of all wealth.

State and local governments are also in dire straits due to the crisis. Their costs have shot up and their tax bases have shrunk. But the Fed’s “special purpose vehicles” were no help. The Municipal Liquidity Facility, ostensibly intended to relieve municipal debt burdens, lent at market interest rates plus a penalty, making borrowing at the facility so expensive that it went nearly unused; and it was discontinued in December.

The Fed’s emergency lending facilities were also of little help to local businesses. In a January 2021 Wall Street Journal article titled “Corporate Debt ‘Relief’ Is an Economic Dud,” Sheila Bair – who is former chair of the Federal Deposit Insurance Corporation, and Lawrence Goodman – president of the Center for Financial Stability, observed:

“ The creation of the corporate facilities last March marked the first time that the Fed would buy corporate debt … The purpose of the corporate facilities was to help companies access debt markets during the pandemic, making it possible to sustain operations and keep employees on payroll.

“ Instead, these facilities resulted in a huge and unnecessary bailout of corp- orate debt issuers, underwriters and bondholders….This created a further unfair opportunity for large corporations to grow bigger by purchasing competitors with government-subsidized credit.

“ …This presents a double whammy for the young companies that have been hit hardest by the pandemic. They are the primary sources of both job creation and innovation, and squeezing them deprives our economy of the dynamism and creativity it needs to thrive. “

In a September 2020 study for ACRE called “Cancel Wall Street,” Saqib Bhatti and Brittany Alston showed that U.S. state and local governments collectively pay $160 billion annually just in interest within the bond market, which is controlled by big private banks. For comparative purposes, $160 billion would be enough to help 13 million families avoid eviction by covering their annual rent; and $134 billion could make up the revenue shortfall suffered by every city and town in the U.S. due to the pandemic.

Half the cost of infrastructure generally consists of financing, doubling its cost to municipal governments. The local governments are extremely good credit risks; yet private, bank-affiliated rating agencies give them a lower credit score (raising their rates) than private corp- orations, which are 63 times more likely to default.

States are not allowed to go bankrupt, and that is also true for cities in about half the states. State and local governments have a tax base ensuring payment of their debts and are not going anywhere, unlike bankrupt corporations, which simply disappear and leave their creditors holding the bag.

How publicly-owned banks can help

Banks do not suffer from the funding problems experienced by local governments. In March 2020, the Federal Reserve reduced the interest rate at its discount window, encouraging all banks in good standing to borrow there at 0.25%. And no stigma or strings were attached to this virtually free liquidity – no need to retain employees or to cut dividends, bonuses, or the interest rates that are charged to borrowers. The Wall Street banks can borrow at a mere one- quarter of one percent while continuing to charge customers 15% or more on their credit cards.

Local governments extend credit to their communities through loan funds, but these “revolving funds” can lend only the capital they have. Depository banks, on the other hand, can leverage their capital, generating up to ten times their capital base in loans.

For a local government with its own depository bank, that would mean up to ten times the credit that can be injected into the local economy, and ten times the profit to be funnelled back into community needs. A public depository bank could also borrow at 0.25% from the Fed’s discount window.

North Dakota leads the way

What a state can achieve by forming its own bank has been demonstrated in North Dakota. There the nation’s only state-owned bank was formed in 1919 when North Dakota farmers were losing their farms to big out-of-state banks.

Unlike the Wall Street megabanks mandated to make as much money as possible for their shareholders, the Bank of North Dakota (BND) is mandated to serve the public interest.

Yet it has had a stellar return on investment, outperforming even J.P. Morgan Chase and Goldman Sachs. In its 2019 Annual Report, the BND reported its sixteenth consecutive year of record profits, with $169 million in income, just over $7 billion in assets, and a hefty return on investment of 18.6%.

The BND maximizes its profits and its ability to serve the community by eliminating profiteering middlemen. It has no private shareholders bent on short-term profits, no high-paid executives, no need to advertise for depositors or borrowers, and no need for multiple branches. It has a massive built-in deposit base, since the state’s revenues must be deposited in the BND by

law. It does not compete with North Dakota’s local banks in the retail market but instead partners with them.

The local bank services and retains the customer, while the BND helps as needed with capital and liquidity. Largely due to this amicable relationship, North Dakota has nearly six times as many local financial institutions per person as the country overall.

The BND has performed particularly well in economic crises. It helped pay the state’s teachers during the Great Depression, and sold foreclosed farmland back to farmers in the 1940s. It has also helped the state recover from a litany of natural disasters.

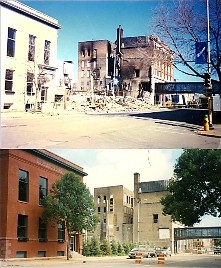

Its emergency capabilities were demonstrated in 1997, when record flooding and fires devastated Grand Forks in North Dakota. The town and its sister city, East Grand Forks located on the Minnesota side of the Red River, lay in ruins. The response of the BND was immediate and comprehensive, demonstrating a financial flexibility and public generosity that no privately-owned bank could match.

The BND quickly established nearly $70 million in credit lines and launched a disaster relief loan program; worked closely with federal agencies to gain forbearance on federally-backed home loans and student loans; and reduced interest rates on existing family farm and farm operating programs.

The BND obtained funds at reduced rates from the Federal Home Loan Bank and passed the savings on to flood-affected borrowers. Grand Forks was quickly rebuilt and restored, losing only 3% of its population by 2000, compared to 17% in East Grand Forks on the other side of the river.

In the 2020 crisis, North Dakota shone again, leading the nation in getting funds into the hands of workers and small businesses.

Unemployment benefits were distributed in North Dakota faster than in any other state, and small businesses also secured more Payroll Protection Program funds per worker than in any other state.

Jeff Stein, writing in May 2020 in The Washington Post, asked:

What’s their secret? Much credit goes to the century-old Bank of North Dakota, which — even before the PPP officially rolled out — coordinated and educated local bankers in weekly conference calls and flurries of calls and emails.

According Eric Hardmeyer, BND’s president and chief executive, BND connected the state’s small bankers with politicians and U.S. Small Business Administration officials and even bought some of their PPP loans to help spread out the cost and risk….

BND has already rolled out two local successor programs to the PPP, intended to help businesses restart and rebuild. It has also offered deferments on its $1.1 billion portfolio of student loans.

Public banks excel globally in crises

Publicly-owned banks around the world have responded quickly and efficiently to crises. As of mid-2020, public banks worldwide held nearly $49 trillion in combined assets; and including other public financial institutions, the figure reached nearly $82 trillion. In a 2020 compendium of case studies titled Public Banks and Covid 19: Combatting the Pandemic with Public Finance, the editors write:

“ Five overarching and promising lessons stand out: public banks have the potential for fast response; to fulfill their public purpose mandate; to act boldly; to mobilize their existing institutional capacity; and to build on ‘public-public’ solidarity. In short, public banks are helping us to navigate the tidal wave of Covid-19 at the same time as private lenders are turning away….

“ Public banks have crafted unprecedented responses to give micro-, small and medium-sized enterprises, large businesses, public entities, governing authorities and households time to breathe, time to adjust and time to over- come the worst of the crisis. Typically, this meant offering liquidity with generously reduced rates of interest, preferential repayment terms and eased conditions of repayment. For the most vulnerable in society, public banks offered non-repayable grants. “

The editors conclude that public banks offer a path toward democratization (giving society a meaningful say in how financial resources are used) and also definancialization (moving away from speculative predatory investment practices toward financing that grows the real economy). For local governments, public banks offer a pathway to evade monopoly control of public policy by giant private financial institutions,

- Source: https://ellenbrown.com/2021/03/04/will-2021-be-public-bankings-watershed-moment/

- https://bsnews.info/wales-needs-consider-following-successful-public-banking-model-north-dakota/

-

https://www.theguardian.com/us-news/2019/oct/03/california-governor-public-banking-law-ab857